%202.svg)

There are two ways to read Armenia’s recent economic story. The first is as a success: after the shockwaves that followed Russian-Ukraine war, Armenia became a fast-growing economy in its region, posting GDP growth of 12.6% in 2022 and 8.3% in 2023. The second is more demanding: much of that boom was powered by temporary inflows such as migration, business relocation, remittances, and trade re-routing that could not be expected to last. Now, as growth moderates, the real question is whether Armenia can turn a windfall into a durable development model. That is the challenge at the heart of the World Bank’s Armenia Country Economic Update (Fall 2025): Fairer Markets for Inclusive Growth. Source

Recent Economic Performance: From Recovery to Acceleration

Armenia entered the 2020s with moderate but steady growth. After a recovery phase in 2021, the country experienced an exceptional economic expansion in 2022 and 2023. Growth reached double digits in 2022 and remained strong in 2023, placing Armenia among the fastest-growing economies in its region.

Why Armenia’s boom was real but temporary

Armenia’s boom reflected real economic activity, rising demand, expanding services, stronger consumption, and a burst of financial and trade flows. Following the war in Ukraine, Armenia benefited from a sharp increase in arrivals from Russia, relocation of firms especially in ICT, surging remittances, and a rapid expansion in trade intermediation.

One of the most immediate effects was the inflow of migrants, particularly from Russia. Many of these individuals were skilled professionals, especially in the IT and service sectors. Their arrival boosted demand for housing, services, and local goods, while also contributing to the expansion of Armenia’s growing tech ecosystem. This combination of increased consumption and enhanced human capital created a powerful short-term stimulus.

At the same time, Armenia experienced a surge in financial inflows. Bank deposits grew, money transfers increased, and overall liquidity in the financial system improved. These developments supported both consumption and investment, further accelerating economic activity.

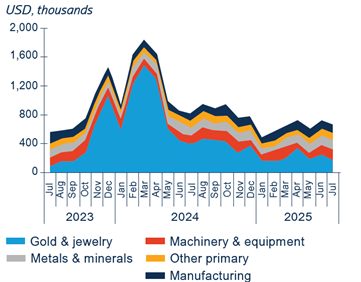

Trade dynamics also shifted notably. Armenia emerged as an important intermediary in regional trade, particularly through re-export activities. Goods such as electronics, machinery, and vehicles were imported and then re-exported to neighboring markets. This created new opportunities for businesses involved in logistics, trade, and distribution, contributing to a sharp increase in trade turnover.

Net FDI rose to 4.7% of GDP in 2022, remittances peaked at10.3% of GDP, and trade with Russia accelerated as Armenia became a conduit for goods and capital moving through a disrupted regional system.

A growth model powered by extraordinary external disruption is, by definition, hard to sustain once the disruption normalizes. That is precisely what the World Bank now documents. Growth began to normalize in 2024as GDP growth eased to to 5.9% in 2024, then to 5.2% in 2025, before forecasted4.7% by 2027. Those are still healthy numbers, but they mark a clear transition: Armenia is moving from externally amplified growth to a phase where domestic productivity and private-sector quality matter much more.

2024–2025: A Gradual Normalization

As the extraordinary conditions of 2022–2023 began to ease, Armenia’s economy entered a new phase. Growth remained positive but moderated to more sustainable levels. This shift reflects a natural adjustment as temporary inflows of capital and people stabilized.

Remittances and financial inflows returned closer to historical norms, and the pace of re-export activity slowed. At the same time, inflation dynamics changed significantly. After peaking in 2022, inflation declined rapidly and even entered deflationary territory in 2024, largely driven by falling food prices. While this supported household purchasing power, it also indicated softer demand conditions.

That shift does not mean Armenia has run out of strengths. Services are still performing well, with ICT and finance remaining important growth pillars. Construction is expanding rapidly. Private consumption has remained supportive, and investment has also helped offset weaker net exports. The banking sector remains sound, with strong capital buffers and low non-performing loans. Inflation, after staying unusually low in 2024, has moved back toward the Central Bank’s 3% target. In short, the economy remains resilient. But resilience is not the same as dynamism. The question for the next two years is whether Armenia can move from a high-growth moment to a high-productivity economy.

The real constraint: weak competition and a less dynamic private sector

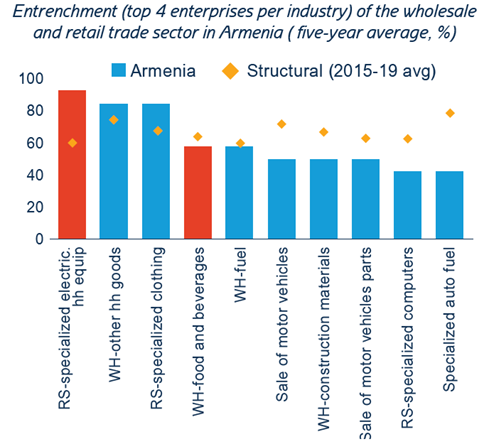

This is where the report becomes especially important. Armenia’s next growth phase will not be secured by short-term demand alone. It depends on whether the private sector is competitive enough to allocate capital well, reward innovation, and allow productive firms to grow. The World Bank’s answer is cautious at best. It finds that labor productivity across sectors remains below that of regional peers. Private investment is weak. Skills shortages persist. And, crucially, market concentration in parts of the economy especially wholesale and retail, including food retail appears to be limiting competition and slowing productivity gains.

The retail findings are especially striking. In food retail, market power appears persistent and entrenched. In Yerevan, a handful of chains dominate store coverage and urban presence. Many supermarkets face no direct competitor within a short walking radius, creating localized pockets of weak competition. This matters because concentrated retail markets do more than shape consumer choice; they also shape the prospects of smaller suppliers, new entrants, and domestic firms trying to scale. When shelf access, payments, and purchasing terms are tilted toward incumbents, the wider private sector becomes less dynamic.

The report also points to supplier-retailer imbalances that can discourage entrepreneurship. Smaller producers and MSMEs may face delayed payments, opaque commercial conditions, slotting fees, and pressure from vertically integrated chains with stronger bargaining power. In those conditions, market access becomes a competitive barrier in itself. Over time, that can reduce product diversity, weaken incentives to invest, and leave consumers paying more while innovation slows. The issue is not simply fairness. It is efficiency. An economy cannot unlock private-sector dynamism if too much advantage sits with a narrow group of incumbents.

What Armenia should do next: a practical reform agenda

If Armenia wants stronger private-sector growth in 2026 and2027, the report suggests a relatively clear agenda.

The first priority is to strengthen competition enforcement. That means giving the Competition and Consumer Protection Commission more resources, stronger analytical capacity, and better digital tools. Modern competition policy depends on data: pricing patterns, market shares, supplier relationships, and geographic concentration. A regulator with limited staffing and weak monitoring tools will always struggle against increasingly sophisticated business structures. Armenia does not need symbolic enforcement; it needs a smarter enforcement state.

The second priority is to rebalance supplier-retailer relations. The report points toward international models such as European rules on unfair trading practices and grocery-sector codes that could help curb abusive commercial practices. Armenia should look seriously at clearer standards for payment periods, slotting fees, return policies, and complaint mechanisms. If MSMEs are expected to drive diversification and job creation, they need a route into markets that is commercially realistic, not structurally stacked against them.

Third, Armenia should improve market transparency. Better public data on customs values, wholesale prices, import flows, and retail prices would help identify where price pass-through is weak and where concentration may be distorting consumer outcomes. Digital price-monitoring tools could support both policymakers and consumers. In a context where food inflation matters deeply for living standards, transparency itself becomes part of the growth strategy.

Fourth, the country needs to crowd in more productive investment. Armenia’s recent boom masked the weakness of underlying FDI and the persistence of structural bottlenecks. Infrastructure, logistics, skills, and regulatory predictability still matter enormously. ICT will remain a major asset, but Armenia cannot rely on one sector alone. A stronger growth model would broaden into higher-value services, more competitive commerce, better connected logistics, and productivity gains in sectors that employ larger shares of the population.

Over the next year or two, the baseline outlook is still favorable by regional standards. Growth should remain solid, inflation broadly manageable, and the banking system supportive. There are upside possibilities too: reduced regional tensions, stronger external integration, and new investment projects could all help. But the risks are real. Geopolitical uncertainty, softer external demand, trade disruption, and pre-election policy uncertainty could all weigh on confidence. That is exactly why structural reform matters now. When the easy gains are gone, the quality of institutions and markets becomes decisive.

A sharper conclusion for Armenia’s next chapter

Armenia’s post-2022 surge was impressive, but the country’s most important economic test is only beginning. The boom proved that Armenia can absorb capital, talent, and opportunity quickly. The next phase will prove whether it can translate those gains into a more competitive and inclusive economy. That means moving beyond the logic of temporary inflows and focusing on the harder work of market reform: stronger competition, fairer supplier relationships, deeper productivity, and better conditions for investment.

After the boom, Armenia does not need nostalgia for extraordinary growth. It needs a new growth engine. If policymakers can use this moment to unlock private-sector dynamism, the slowdown now underway may turn out to be less a loss of momentum than the start of a healthier, more durable expansion.

.png)

.png)